Page 8 - Danir_Klimatbokslut_digital_2022_ENG_240122

P. 8

CHAPTER 3 | Danir GHG inventory report 2022 8

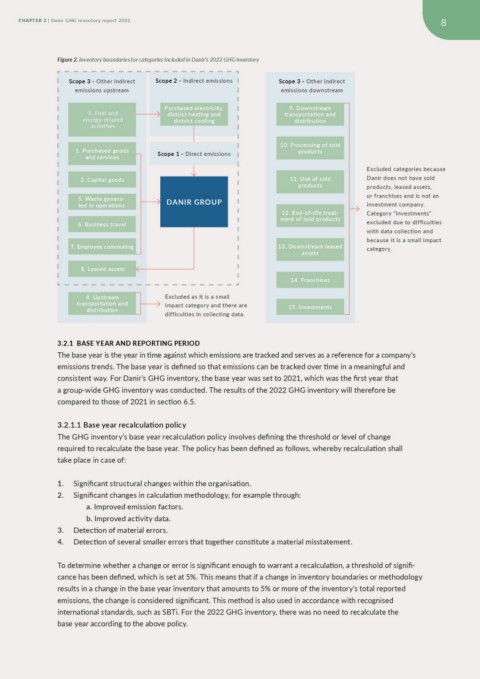

Figure 2. Inventory boundaries for categories included in Danir’s 2022 GHG inventory

Scope 3 - Other indirect Scope 2 - Indirect emissions Scope 3 - Other indirect

emissions upstream emissions downstream

Purchased electricity,

3. Fuel and district heating and 9. Downstream

energy-related district cooling transportation and

activities distribution

1. Purchased goods Scope 1 - Direct emissions 10. Processing of sold Excluded categories because

and services products Danir does not have sold

DANIR GROUP products, leased assets,

2. Capital goods 11. Use of sold or franchises and is not an

5. Waste genera- products investment company.

ted in operations Category “Investments”

6. Business travel 12. End-of-life treat- excluded due to difficulties

ment of sold products with data collection and

7. Employee commuting because it is a small impact

13. Downstream leased category.

8. Leased assets assets

4. Upstream Excluded as it is a small 14. Franchises

transportation and impact category and there are

difficulties in collecting data. 15. Investments

distribution

3.2.1 BASE YEAR AND REPORTING PERIOD

The base year is the year in time against which emissions are tracked and serves as a reference for a company’s

emissions trends. The base year is defined so that emissions can be tracked over time in a meaningful and

consistent way. For Danir’s GHG inventory, the base year was set to 2021, which was the first year that

a group-wide GHG inventory was conducted. The results of the 2022 GHG inventory will therefore be

compared to those of 2021 in section 6.5.

3.2.1.1 Base year recalculation policy

The GHG inventory’s base year recalculation policy involves defining the threshold or level of change

required to recalculate the base year. The policy has been defined as follows, whereby recalculation shall

take place in case of:

1. Significant structural changes within the organisation.

2. Significant changes in calculation methodology, for example through:

a. Improved emission factors.

b. Improved activity data.

3. Detection of material errors.

4. Detection of several smaller errors that together constitute a material misstatement.

To determine whether a change or error is significant enough to warrant a recalculation, a threshold of signifi-

cance has been defined, which is set at 5%. This means that if a change in inventory boundaries or methodology

results in a change in the base year inventory that amounts to 5% or more of the inventory's total reported

emissions, the change is considered significant. This method is also used in accordance with recognised

international standards, such as SBTi. For the 2022 GHG inventory, there was no need to recalculate the

base year according to the above policy.